ICHRA vs Group Health Insurance: A Comprehensive Guide

In the evolving health benefits landscape, employers are increasingly exploring options like Individual Coverage HRAs (ICHRA) as alternatives to traditional group health insurance. At CFH Insurance Consultants, we understand the nuances of each approach to help mid-size employers make informed decisions. ICHRA offers a flexible and cost-controlled solution that empowers employees to choose their own health plans, while traditional group health insurance provides the comfort of comprehensive coverage. Understanding the specific eligibility rules and contribution limits for ICHRA and group health plans is critical for aligning benefits with workforce needs.

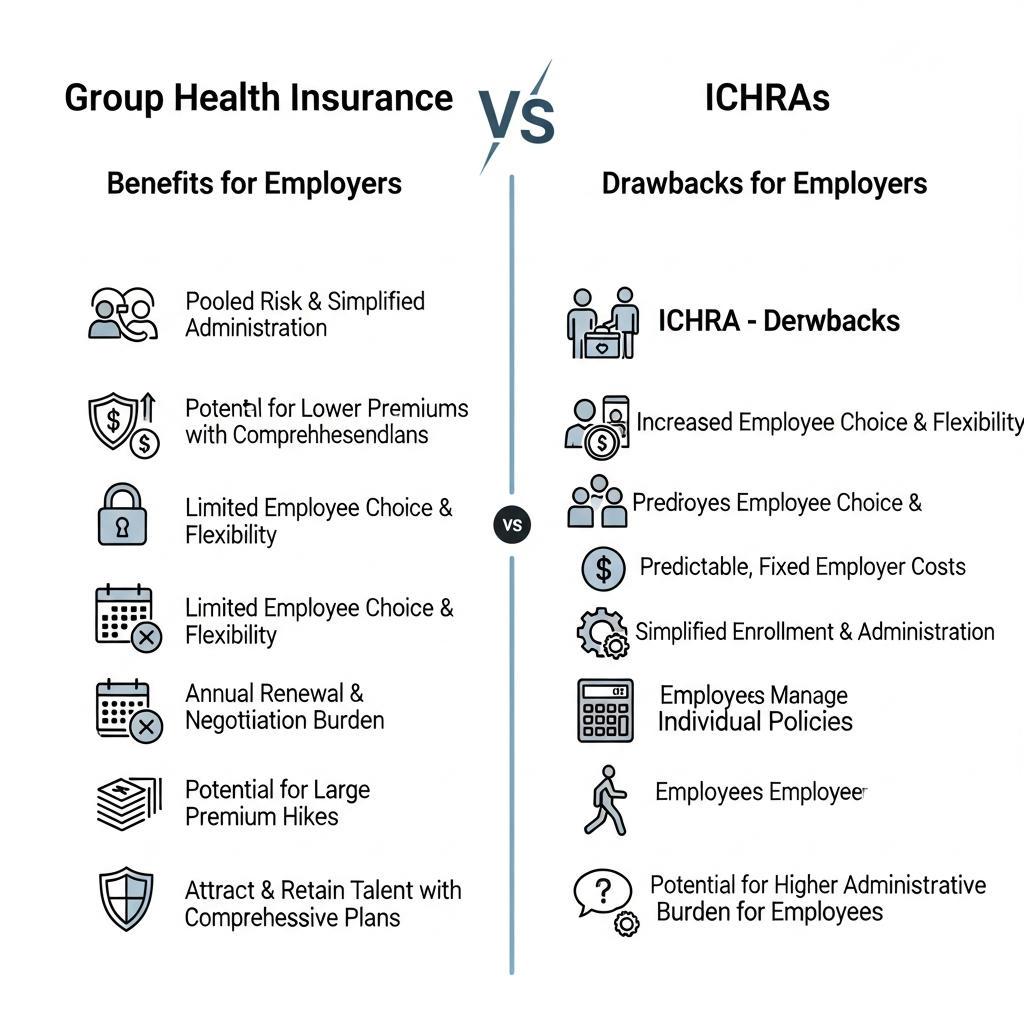

ICHRA vs Group Health Insurance: An In-Depth Comparison

Our core competencies

Understanding ICHRA

Individual Coverage Health Reimbursement Arrangements (ICHRA) provide employers with greater flexibility in defining their health benefits. Unlike traditional group health insurance, ICHRA allows employers to provide a defined contribution to employees, who then purchase their own individual health insurance plans. This approach caters to diverse employee needs while controlling costs for employers. However, it requires a solid understanding of the eligibility requirements and compliance guidelines to ensure ACA regulations are met. Employers must consider their workforce demographics when evaluating ICHRA as a viable option.

Learn More →

Pros and Cons of Group Health Insurance

Group health insurance remains a traditional favorite for many employers due to its comprehensive coverage. It provides a safety net for all employees under the same plan, which fosters a sense of unity and accessibility. However, group health insurance can be costly, with premium increases driven by claims and market conditions. Additionally, the rigid plan designs may not cater to the diverse needs of individual employees. Choosing group insurance often leads to less predictable costs for employers compared to ICHRA, which offers more control and flexibility.

Learn More →

The Role of QSEHRA for Smaller Employers

For smaller employers, the Qualified Small Employer HRA (QSEHRA) presents a compelling alternative to both group health insurance and ICHRA. QSEHRA allows participating employers to reimburse employees for their individual health insurance premiums and out-of-pocket expenses. This option is particularly attractive for those with fewer than 50 employees, providing a more tailored benefits solution without the financial commitment of group plans. Understanding QSEHRA and how it complements ICHRA can position employers with up to 500 employees for competitive advantages in hiring and retention.

Learn More →Common Questions

ICHRA stands for Individual Coverage Health Reimbursement Arrangement, allowing employers to reimburse employees for individual health insurance premiums and qualified medical expenses.

Eligibility for ICHRA depends on the employer's choice, as they can decide how to group employees, whether by full-time status or other categories.

ICHRA offers flexibility and cost control for employers, while traditional group health insurance provides comprehensive coverage for all employees under one plan.

Group health insurance provides broad coverage, often with lower premiums due to pooling risk among many employees, fostering a sense of community.

QSEHRA is a Qualified Small Employer Health Reimbursement Arrangement designed for small employers (under 50 employees) to reimburse health expenses.