Comprehensive ACA Compliance Solutions for Michigan Businesses

Navigating the complexities of ACA compliance can be a challenge for small businesses in Michigan. At CFH Insurance Consultants (CFHIC), we specialize in guiding companies through the intricate landscape of health insurance compliance Michigan requires. Our team helps employers understand their Applicable Large Employer (ALE) status and the associated employer health insurance requirements Michigan mandates. With our expertise, you can ensure your business meets all necessary compliance standards while optimizing benefits expenditure. As a trusted partner for businesses in Bloomfield Hills, Troy, Birmingham, Rochester Hills, and the Detroit metro area, our commitment is to simplify your health insurance compliance journey. CFHIC provides tailored solutions that address minimum value and affordability requirements, utilizing safe harbor methods to protect your business. We also focus on preventing common compliance mistakes that could lead to significant penalties. Let us assist you with annual compliance reviews and streamline your ACA strategy for a better tomorrow.

Understanding ACA Compliance for Michigan Employers

Our core competencies

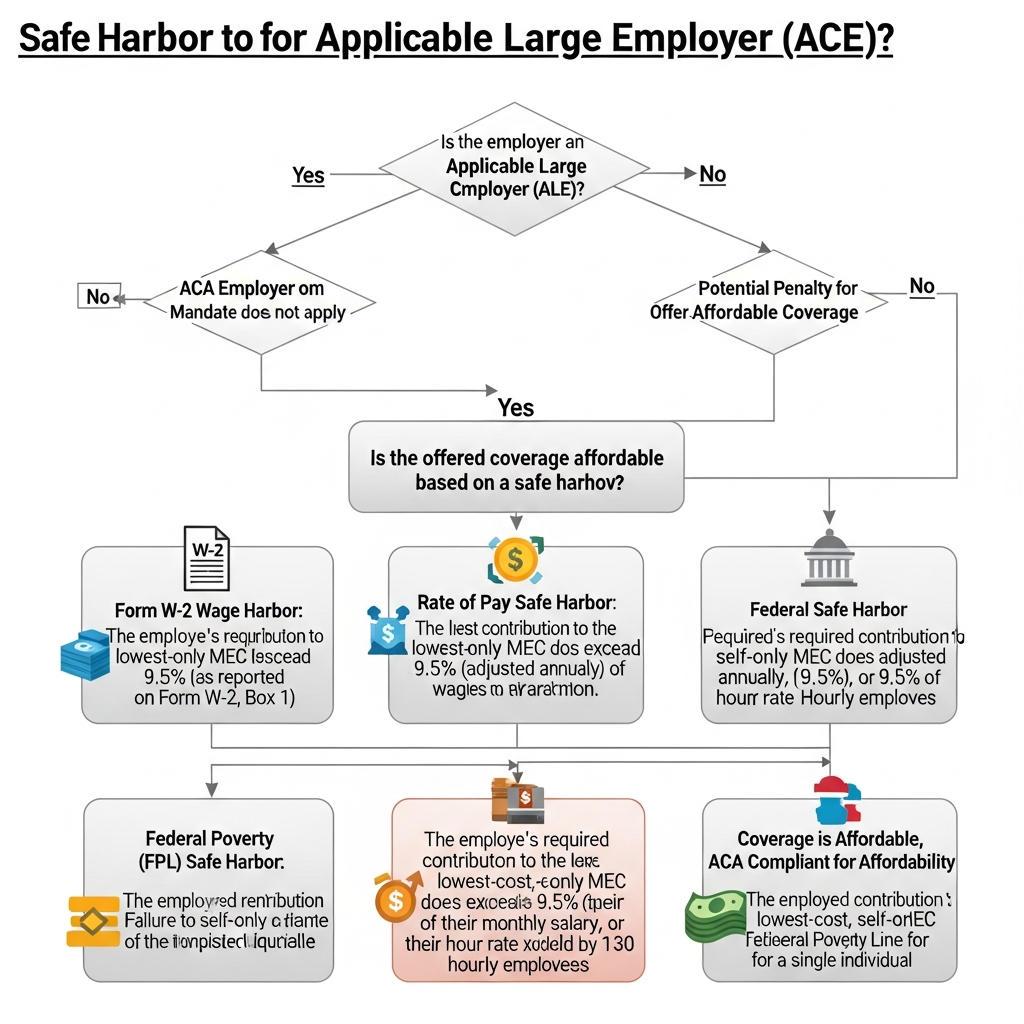

Determining Applicable Large Employer (ALE) Status

Understanding if your business meets the criteria for ALE status is crucial for compliance with the ACA. This determination affects how you approach employer health insurance requirements in Michigan. CFH Insurance Consultants (CFHIC) assists small to mid-sized businesses in evaluating their ALE status, ensuring that compliance with health insurance mandates is both effective and efficient. We provide tailored insights to help highlight your obligations under the law and avoid common pitfalls that could expose your business to penalties.

Learn More →

Minimum Value and Affordability Requirements

To meet ACA compliance standards, Michigan businesses must ensure that their health insurance plans provide minimum value and affordability. CFHIC specializes in helping employers assess their health plans against these criteria. Our guidance on these requirements means you can make informed decisions about health insurance offerings, thereby safeguarding your business from compliance issues. Understanding these elements not only establishes your compliance but also enhances employee retention and satisfaction.

Learn More →

Safe Harbor Methods to Ensure Compliance

Employers in Michigan can utilize safe harbor methods to simplify the ACA compliance process. By working with CFH Insurance Consultants, you'll understand how these methods can shield your business from costly penalties while ensuring your health coverage aligns with ACA standards. We provide detailed guidance on the various safe harbor options available, allowing for greater flexibility in meeting the employer health insurance requirements Massachusetts businesses face.

Learn More →Common Questions

ALE status applies to businesses that have 50 or more full-time employees or full-time equivalent employees. This status determines your health insurance compliance obligations under the ACA.

At CFHIC, we provide comprehensive compliance reviews, guidance on ALE status, minimum value and affordability requirements, and support for using safe harbor methods to ensure your business meets ACA mandates.

The minimum value requirement ensures that a health insurance plan covers at least 60% of average medical costs. The affordability requirement means that employee premiums must be affordable relative to their household income.

Common mistakes include miscalculating ALE status, failing to offer minimum essential coverage, and incorrect reporting to the IRS. These errors can lead to penalties and increased scrutiny.

At least annually, businesses should conduct compliance reviews to ensure they remain updated on ACA requirements and avoid potential penalties.